Thailand is positioning itself as a regional aviation powerhouse, with bold ambitions to become Southeast Asia’s premier hub for air transport, logistics and Maintenance, Repair and Overhaul (MRO) services. Backed by strong government support, major infrastructure investments and increasing regional air traffic, the country is steadily advancing toward this goal.

Central to this vision is the development of U-Tapao International Airport, part of the Eastern Airport City under the Eastern Economic Corridor (EEC). This project will not only increase airport capacity but also anchor a fully integrated aerospace and logistics ecosystem. Alongside U-Tapao, major expansions are underway at Suvarnabhumi and Don Mueang airports, including new terminals, additional runways, MRO hangars, and advanced automation systems, all intended to accommodate the rapid growth in passenger and cargo volumes. For example, Suvarnabhumi’s newly installed Midfield Satellite Terminal 1 adds 28 aircraft stands and will serve up to 60 million passengers, while Don Mueang’s new Terminal 3 will increase capacity to 40 million annual passengers by 2032.

In addition to Bangkok and the Eastern Economic Corridor, the Thai government and the Airports of Thailand (AOT) are investing in provincial airport upgrades across the country. Airports in Chiang Mai, Phuket, Hat Yai and Khon Kaen are undergoing expansion and modernization to meet increasing demand. These regional improvements aim to decentralize air traffic, reduce congestion at the capital’s two airports and better support Thailand’s regional tourism and logistics ambitions. Strengthening these airports also enhances Thailand’s readiness to serve as a multi-node aviation hub, connecting travelers and cargo across Southeast Asia with greater flexibility and resilience.

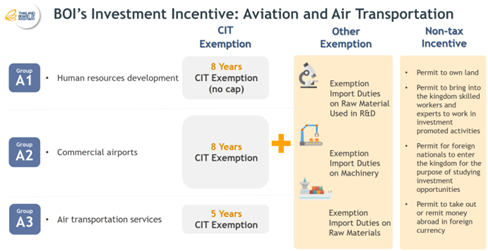

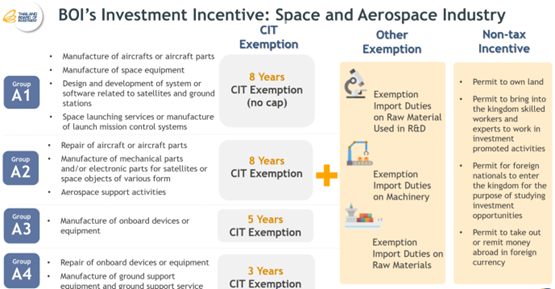

The government’s commitment is not just physical. Through the Board of Investment (BOI), Thailand offers attractive incentives for aviation and aerospace companies, ranging from corporate tax exemptions of up to 13 years, to import duty waivers and 100% foreign ownership rights. These policies are part of a national strategy to attract global players in aircraft manufacturing, aircraft parts and space-related technologies.

Importantly, Thailand is already home to several global OEMs and has demonstrated strength in the aviation supply chain. What gives Thailand an edge over regional competitors like Malaysia or Vietnam is its strategic location, well-established safety standards and a robust logistics network. The country’s resilience, skilled workforce and political commitment to becoming an aviation and logistics hub further reinforce its competitive positioning.

However, several challenges remain. The success of large-scale aviation projects depend heavily on the coordination between public and private stakeholders. Regulatory delays, procurement bottlenecks and land use issues could slow down progress. Moreover, while infrastructure is expanding rapidly, workforce development in highly specialized aviation fields, such as MRO engineering and digital airport systems needs to keep pace. Competition is also intensifying in the region, with countries like Singapore, Vietnam and the Philippines aggressively enhancing their own aviation offerings. Additionally, geopolitical uncertainties and economic headwinds could influence foreign investment and airline route planning in the years ahead.

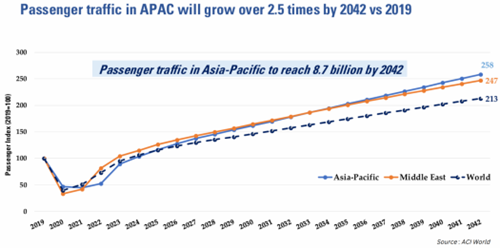

This being said, Passenger traffic in Asia-Pacific is expected to more than double by 2042, and Thailand is determined to ride this wave. As the region’s aviation landscape continues to shift eastward, Thailand’s combination of infrastructure, incentives and strategy places it in a strong position, not only to serve as a travel hub but to drive aerospace innovation and industrial growth.

In short, Thailand isn’t just expanding airports, it’s building a future-ready aviation ecosystem, while navigating the complex challenges that come with ambition on a regional scale.